Mobile

Mobile

Mobile

Personal project

Personal project

Personal project

Fintech

Fintech

Fintech

No more awkward money talks: fixing bill splitting with UX

No more awkward money talks: fixing bill splitting with UX

No more awkward money talks: fixing bill splitting with UX

No more awkward money talks: fixing bill splitting with UX

No more awkward money talks: fixing bill splitting with UX

No more awkward money talks: fixing bill splitting with UX

You just paid for dinner with friends. Now comes the awkward part: figuring out who owes what, chasing payments, and hoping no one ‘forgets.’

Expense-sharing should be simple, but the reality is often messy.

This case study examines how a well-designed fintech solution can transform bill-splitting from a source of friction into an effortless, automated process—protecting both users' wallets and their friendships.

You just paid for dinner with friends. Now comes the awkward part: figuring out who owes what, chasing payments, and hoping no one ‘forgets.’

Expense-sharing should be simple, but the reality is often messy.

This case study examines how a well-designed fintech solution can transform bill-splitting from a source of friction into an effortless, automated process—protecting both users' wallets and their friendships.

You just paid for dinner with friends. Now comes the awkward part: figuring out who owes what, chasing payments, and hoping no one ‘forgets.’

Expense-sharing should be simple, but the reality is often messy.

This case study examines how a well-designed fintech solution can transform bill-splitting from a source of friction into an effortless, automated process—protecting both users' wallets and their friendships.

You just paid for dinner with friends. Now comes the awkward part: figuring out who owes what, chasing payments, and hoping no one ‘forgets.’

Expense-sharing should be simple, but the reality is often messy.

This case study examines how a well-designed fintech solution can transform bill-splitting from a source of friction into an effortless, automated process—protecting both users' wallets and their friendships.

You just paid for dinner with friends. Now comes the awkward part: figuring out who owes what, chasing payments, and hoping no one ‘forgets.’

Expense-sharing should be simple, but the reality is often messy.

This case study examines how a well-designed fintech solution can transform bill-splitting from a source of friction into an effortless, automated process—protecting both users' wallets and their friendships.

You just paid for dinner with friends. Now comes the awkward part: figuring out who owes what, chasing payments, and hoping no one ‘forgets.’

Expense-sharing should be simple, but the reality is often messy.

This case study examines how a well-designed fintech solution can transform bill-splitting from a source of friction into an effortless, automated process—protecting both users' wallets and their friendships.

1-month

Timeline

Product designer

Role

Me + AI assistant

Team

1-month

Timeline

Product designer

Role

Me + AI assistant

Team

Solution

Problem statement

Managing shared expenses among friends, family, or roommates often leads to frustration due to unequal contributions, delayed payments, and financial misunderstandings. Research indicates that these challenges are widespread and time-consuming, adding unnecessary stress to users’ financial management.

Negative experience with cost-sharing

73%

of GenZ individuals

Cash App survey

Having arguments over splitting costs

42%

of GenZ individuals

Cash App survey

A Cash App survey revealed that:

73% of Gen Z individuals (aged 16-26) have had at least one negative experience with cost-sharing among friends. On top of that, 42% of Gen Z respondents reported having arguments with friends over splitting costs. (source: ypulse report).

This indicates a significant need for better solutions in expense sharing: one with a user-friendly automatic reminder feature—to not only save money but friendships as well.

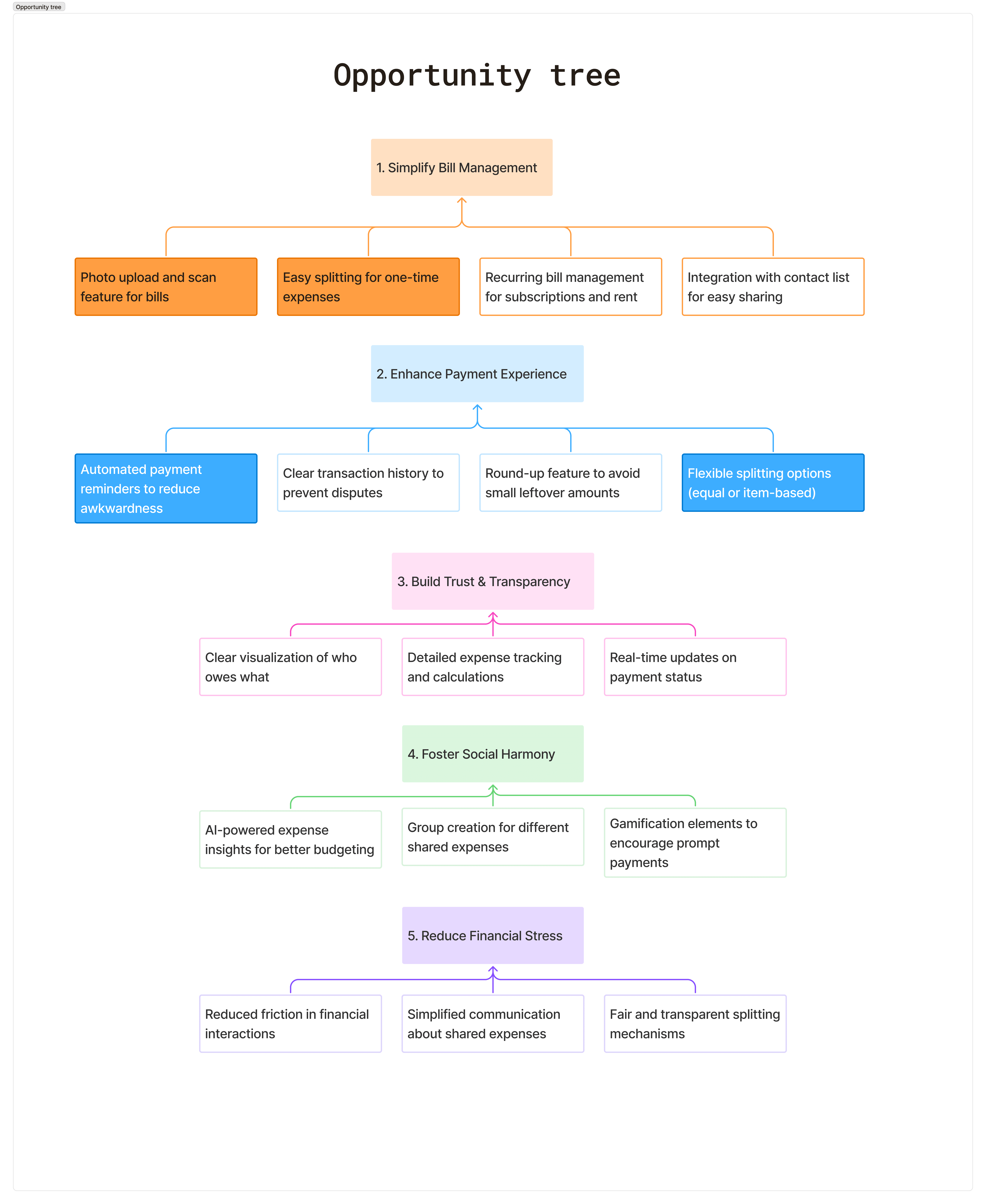

Business opportunity

As designers, we need to grasp the business factors, variables, and constraints that impact the success of our design work. This means focusing on features and services that have the greatest business potential. I like organizing the potential areas of opportunities into an opportunity tree. It enables easy contrast and comparison of ideas.

Opportunity tree

I followed upon the opportunities that promised the greatest leverage for the business:

1

Photo upload and scan feature for bills

Not many services offer this feature, we could have a unique edge here, scanned bill enables users to split the costs fairly based on consumption.

2

Easy splitting for one-time expenses

If done right, it boosts user engagement with the app and potentially attract more customers through social proof.

3

Automated payment reminders to reduce awkwardness

Many users sets up reminders for themselves to remind others to pay them back, others just forget. This sounds like a real pain reliever business opportunity.

4

Flexible splitting options (equal or item-based)

While most bill splitting apps provide equal split, item-based splitting is the norm in many countries, like Germany or the Netherlands. Offering a frictionless option for an item-based splitting is a real business opportunity.

Solutions

My guiding principles

1

Simplifying complexity

Turning intricate financial workflows into intuitive path suitable for the general public Playfulness achieved by powder colors and sharp shadows to want them to use the app

2

Mobile-first interaction

GenZ was born with smart phones in their hands. They do most of their digital activities through mobile, on the go. Haptics, feedbacks, accessibility are key for success. Responsiveness (low data mode)

3

Accessibility & trust

Fintech users need clarity and confidence. The interface should support and reflect this. I achieved that with well chosen typography, strong enough contrast that passes the WCAG standards and by applying micro-interactions that reinforces trust.

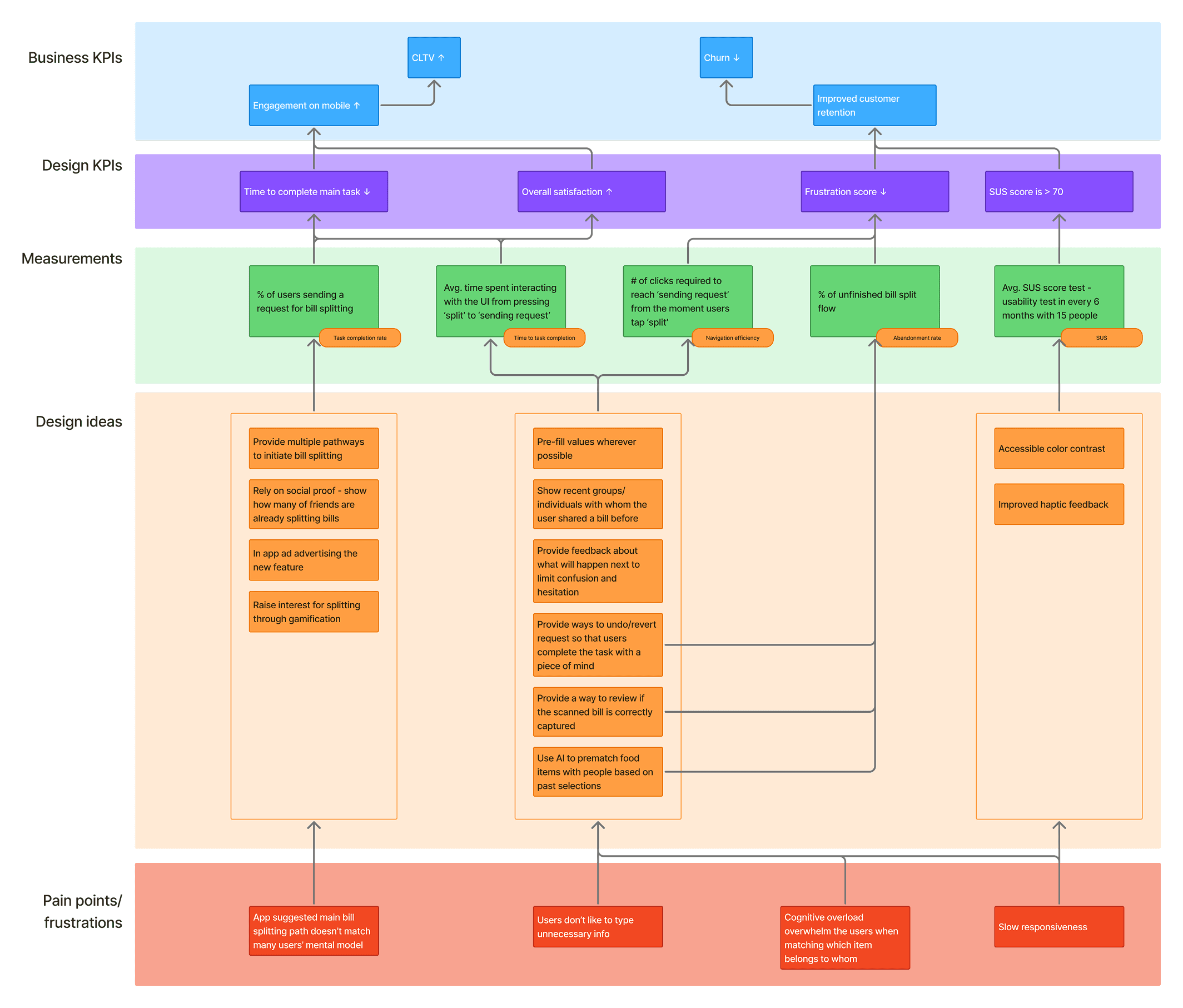

Business impact

Even though this was a fictive project, hence there are no real business benefit to show, it is still worth showing how the UX improvement efforts would contribute to the business objectives. One can do that by building a KPI tree. By connecting the observed usability issues with design ideas and metrics we can track if the UX changes were effective.

Conclusion

The real UX challenge is not how to split bills easily—it’s building systems for young individuals that promotes and teaches financial literacy and help sustaining a healthy financial habit. Starting with sharing costs, and encouraging them to pay each other back on time. Behavioral insights and strategies ensure that financial tools aren’t just another app on someone’s phone but become part of how people live their financial lives.

Solution

Problem statement

Managing shared expenses among friends, family, or roommates often leads to frustration due to unequal contributions, delayed payments, and financial misunderstandings. Research indicates that these challenges are widespread and time-consuming, adding unnecessary stress to users’ financial management.

Negative experience with cost-sharing

73%

of GenZ individuals

Cash App survey

Having arguments over splitting costs

42%

of GenZ individuals

Cash App survey

A Cash App survey revealed that:

73% of Gen Z individuals (aged 16-26) have had at least one negative experience with cost-sharing among friends. On top of that, 42% of Gen Z respondents reported having arguments with friends over splitting costs. (source: ypulse report).

This indicates a significant need for better solutions in expense sharing: one with a user-friendly automatic reminder feature—to not only save money but friendships as well.

Business opportunity

As designers, we need to grasp the business factors, variables, and constraints that impact the success of our design work. This means focusing on features and services that have the greatest business potential. I like organizing the potential areas of opportunities into an opportunity tree. It enables easy contrast and comparison of ideas.

Opportunity tree

I followed upon the opportunities that promised the greatest leverage for the business:

1

Photo upload and scan feature for bills

Not many services offer this feature, we could have a unique edge here, scanned bill enables users to split the costs fairly based on consumption.

2

Easy splitting for one-time expenses

If done right, it boosts user engagement with the app and potentially attract more customers through social proof.

3

Automated payment reminders to reduce awkwardness

Many users sets up reminders for themselves to remind others to pay them back, others just forget. This sounds like a real pain reliever business opportunity.

4

Flexible splitting options (equal or item-based)

While most bill splitting apps provide equal split, item-based splitting is the norm in many countries, like Germany or the Netherlands. Offering a frictionless option for an item-based splitting is a real business opportunity.

Solutions

My guiding principles

1

Simplifying complexity

Turning intricate financial workflows into intuitive path suitable for the general public Playfulness achieved by powder colors and sharp shadows to want them to use the app

2

Mobile-first interaction

GenZ was born with smart phones in their hands. They do most of their digital activities through mobile, on the go. Haptics, feedbacks, accessibility are key for success. Responsiveness (low data mode)

3

Accessibility & trust

Fintech users need clarity and confidence. The interface should support and reflect this. I achieved that with well chosen typography, strong enough contrast that passes the WCAG standards and by applying micro-interactions that reinforces trust.

Business impact

Even though this was a fictive project, hence there are no real business benefit to show, it is still worth showing how the UX improvement efforts would contribute to the business objectives. One can do that by building a KPI tree. By connecting the observed usability issues with design ideas and metrics we can track if the UX changes were effective.

Conclusion

The real UX challenge is not how to split bills easily—it’s building systems for young individuals that promotes and teaches financial literacy and help sustaining a healthy financial habit. Starting with sharing costs, and encouraging them to pay each other back on time. Behavioral insights and strategies ensure that financial tools aren’t just another app on someone’s phone but become part of how people live their financial lives.

Solution

Problem statement

Managing shared expenses among friends, family, or roommates often leads to frustration due to unequal contributions, delayed payments, and financial misunderstandings. Research indicates that these challenges are widespread and time-consuming, adding unnecessary stress to users’ financial management.

Negative experience with cost-sharing

73%

of GenZ individuals

Cash App survey

Having arguments over splitting costs

42%

of GenZ individuals

Cash App survey

A Cash App survey revealed that:

73% of Gen Z individuals (aged 16-26) have had at least one negative experience with cost-sharing among friends. On top of that, 42% of Gen Z respondents reported having arguments with friends over splitting costs. (source: ypulse report).

This indicates a significant need for better solutions in expense sharing: one with a user-friendly automatic reminder feature—to not only save money but friendships as well.

Business opportunity

As designers, we need to grasp the business factors, variables, and constraints that impact the success of our design work. This means focusing on features and services that have the greatest business potential. I like organizing the potential areas of opportunities into an opportunity tree. It enables easy contrast and comparison of ideas.

Opportunity tree

I followed upon the opportunities that promised the greatest leverage for the business:

1

Photo upload and scan feature for bills

Not many services offer this feature, we could have a unique edge here, scanned bill enables users to split the costs fairly based on consumption.

2

Easy splitting for one-time expenses

If done right, it boosts user engagement with the app and potentially attract more customers through social proof.

3

Automated payment reminders to reduce awkwardness

Many users sets up reminders for themselves to remind others to pay them back, others just forget. This sounds like a real pain reliever business opportunity.

4

Flexible splitting options (equal or item-based)

While most bill splitting apps provide equal split, item-based splitting is the norm in many countries, like Germany or the Netherlands. Offering a frictionless option for an item-based splitting is a real business opportunity.

Solutions

My guiding principles

1

Simplifying complexity

Turning intricate financial workflows into intuitive path suitable for the general public Playfulness achieved by powder colors and sharp shadows to want them to use the app

2

Mobile-first interaction

GenZ was born with smart phones in their hands. They do most of their digital activities through mobile, on the go. Haptics, feedbacks, accessibility are key for success. Responsiveness (low data mode)

3

Accessibility & trust

Fintech users need clarity and confidence. The interface should support and reflect this. I achieved that with well chosen typography, strong enough contrast that passes the WCAG standards and by applying micro-interactions that reinforces trust.

Business impact

Even though this was a fictive project, hence there are no real business benefit to show, it is still worth showing how the UX improvement efforts would contribute to the business objectives. One can do that by building a KPI tree. By connecting the observed usability issues with design ideas and metrics we can track if the UX changes were effective.

Conclusion

The real UX challenge is not how to split bills easily—it’s building systems for young individuals that promotes and teaches financial literacy and help sustaining a healthy financial habit. Starting with sharing costs, and encouraging them to pay each other back on time. Behavioral insights and strategies ensure that financial tools aren’t just another app on someone’s phone but become part of how people live their financial lives.

Solution

Problem statement

Managing shared expenses among friends, family, or roommates often leads to frustration due to unequal contributions, delayed payments, and financial misunderstandings. Research indicates that these challenges are widespread and time-consuming, adding unnecessary stress to users’ financial management.

Negative experience with cost-sharing

73%

of GenZ individuals

Cash App survey

Having arguments over splitting costs

42%

of GenZ individuals

Cash App survey

A Cash App survey revealed that:

73% of Gen Z individuals (aged 16-26) have had at least one negative experience with cost-sharing among friends. On top of that, 42% of Gen Z respondents reported having arguments with friends over splitting costs. (source: ypulse report).

This indicates a significant need for better solutions in expense sharing: one with a user-friendly automatic reminder feature—to not only save money but friendships as well.

Business opportunity

As designers, we need to grasp the business factors, variables, and constraints that impact the success of our design work. This means focusing on features and services that have the greatest business potential. I like organizing the potential areas of opportunities into an opportunity tree. It enables easy contrast and comparison of ideas.

Opportunity tree

I followed upon the opportunities that promised the greatest leverage for the business:

1

Photo upload and scan feature for bills

Not many services offer this feature, we could have a unique edge here, scanned bill enables users to split the costs fairly based on consumption.

2

Easy splitting for one-time expenses

If done right, it boosts user engagement with the app and potentially attract more customers through social proof.

3

Automated payment reminders to reduce awkwardness

Many users sets up reminders for themselves to remind others to pay them back, others just forget. This sounds like a real pain reliever business opportunity.

4

Flexible splitting options (equal or item-based)

While most bill splitting apps provide equal split, item-based splitting is the norm in many countries, like Germany or the Netherlands. Offering a frictionless option for an item-based splitting is a real business opportunity.

Solutions

My guiding principles

1

Simplifying complexity

Turning intricate financial workflows into intuitive path suitable for the general public Playfulness achieved by powder colors and sharp shadows to want them to use the app

2

Mobile-first interaction

GenZ was born with smart phones in their hands. They do most of their digital activities through mobile, on the go. Haptics, feedbacks, accessibility are key for success. Responsiveness (low data mode)

3

Accessibility & trust

Fintech users need clarity and confidence. The interface should support and reflect this. I achieved that with well chosen typography, strong enough contrast that passes the WCAG standards and by applying micro-interactions that reinforces trust.

Business impact

Even though this was a fictive project, hence there are no real business benefit to show, it is still worth showing how the UX improvement efforts would contribute to the business objectives. One can do that by building a KPI tree. By connecting the observed usability issues with design ideas and metrics we can track if the UX changes were effective.

Conclusion

The real UX challenge is not how to split bills easily—it’s building systems for young individuals that promotes and teaches financial literacy and help sustaining a healthy financial habit. Starting with sharing costs, and encouraging them to pay each other back on time. Behavioral insights and strategies ensure that financial tools aren’t just another app on someone’s phone but become part of how people live their financial lives.

Solution

Problem statement

Managing shared expenses among friends, family, or roommates often leads to frustration due to unequal contributions, delayed payments, and financial misunderstandings. Research indicates that these challenges are widespread and time-consuming, adding unnecessary stress to users’ financial management.

Negative experience with cost-sharing

73%

of GenZ individuals

Cash App survey

Having arguments over splitting costs

42%

of GenZ individuals

Cash App survey

A Cash App survey revealed that:

73% of Gen Z individuals (aged 16-26) have had at least one negative experience with cost-sharing among friends. On top of that, 42% of Gen Z respondents reported having arguments with friends over splitting costs. (source: ypulse report).

This indicates a significant need for better solutions in expense sharing: one with a user-friendly automatic reminder feature—to not only save money but friendships as well.

Business opportunity

As designers, we need to grasp the business factors, variables, and constraints that impact the success of our design work. This means focusing on features and services that have the greatest business potential. I like organizing the potential areas of opportunities into an opportunity tree. It enables easy contrast and comparison of ideas.

Opportunity tree

I followed upon the opportunities that promised the greatest leverage for the business:

1

Photo upload and scan feature for bills

Not many services offer this feature, we could have a unique edge here, scanned bill enables users to split the costs fairly based on consumption.

2

Easy splitting for one-time expenses

If done right, it boosts user engagement with the app and potentially attract more customers through social proof.

3

Automated payment reminders to reduce awkwardness

Many users sets up reminders for themselves to remind others to pay them back, others just forget. This sounds like a real pain reliever business opportunity.

4

Flexible splitting options (equal or item-based)

While most bill splitting apps provide equal split, item-based splitting is the norm in many countries, like Germany or the Netherlands. Offering a frictionless option for an item-based splitting is a real business opportunity.

Solutions

My guiding principles

1

Simplifying complexity

Turning intricate financial workflows into intuitive path suitable for the general public Playfulness achieved by powder colors and sharp shadows to want them to use the app

2

Mobile-first interaction

GenZ was born with smart phones in their hands. They do most of their digital activities through mobile, on the go. Haptics, feedbacks, accessibility are key for success. Responsiveness (low data mode)

3

Accessibility & trust

Fintech users need clarity and confidence. The interface should support and reflect this. I achieved that with well chosen typography, strong enough contrast that passes the WCAG standards and by applying micro-interactions that reinforces trust.

Business impact

Even though this was a fictive project, hence there are no real business benefit to show, it is still worth showing how the UX improvement efforts would contribute to the business objectives. One can do that by building a KPI tree. By connecting the observed usability issues with design ideas and metrics we can track if the UX changes were effective.

Conclusion

The real UX challenge is not how to split bills easily—it’s building systems for young individuals that promotes and teaches financial literacy and help sustaining a healthy financial habit. Starting with sharing costs, and encouraging them to pay each other back on time. Behavioral insights and strategies ensure that financial tools aren’t just another app on someone’s phone but become part of how people live their financial lives.

More projects

Introducing a scalable fair image pixel based pricing for cloud processing of photogrammetry datasets

CX designer

Introducing a scalable fair image pixel based pricing for cloud processing of photogrammetry datasets

CX designer

Introducing a scalable fair image pixel based pricing for cloud processing of photogrammetry datasets

CX designer

Introducing a scalable fair image pixel based pricing for cloud processing of photogrammetry datasets

CX designer

Introducing a scalable fair image pixel based pricing for cloud processing of photogrammetry datasets

CX designer

Service design tool: an online tool for designing on-demand transportation services

Visionary fairy tale

Service design tool: an online tool for designing on-demand transportation services

Visionary fairy tale

Service design tool: an online tool for designing on-demand transportation services

Visionary fairy tale

Service design tool: an online tool for designing on-demand transportation services

Visionary fairy tale

Service design tool: an online tool for designing on-demand transportation services

Visionary fairy tale